Record high vegetable oil prices are at or near their peak and the global oils and fats market is likely to see lower prices for the remainder of this year, Oil World executive director Thomas Mielke told the Virtual Price Outlook Conference (POC) 2021 on 24 March.

Mielke said the high vegetable oil prices, which had doubled in the past 12 months, were due to a global production deficit, low stocks and biofuels consumption.

Black Sea sunflower oil prices, for example, had almost doubled to US$1,575/tonne as of 22 March, against US$815/tonne on 3 August 2020.

Palm kernel oil (PKO) had doubled to US$1,480/tonne against US$730/tonne (cif Rotterdam) in the same time period, while Argentine soyabean oil was US$1,253/tonne against US$782/tonne (fob) in the same time frame.

“Indonesian crude palm oil (CPO) more than doubled from US$500/tonne in May 2020 to US$1,130 on 23 March, a nine-year high,” Mielke added.

Despite high prices, palm oil usage in biodiesel and hydrotreated vegetable oil (HVO) was still high at 17.3M tonnes in 2020, which was 23% of total world palm oil consumption.

In 2020, palm oil accounted for 32% of global vegetable oil production, with soyabean oil accounting for 25%.

World production of palm oil was likely to rebound by 3.2M tonnes in Oct/Sept 2020/21. However, low opening stocks, which were down by 2.5M tonnes, would limit supply growth to just 0.7M tonnes.

A key factor facing Malaysia’s palm oil industry was labour shortages, exacerbated by COVID restrictions impacting the recruitment of foreign workers, who account for 70% of the plantation workforce. Other key issues were the lack of replanting and a declining yield trend.

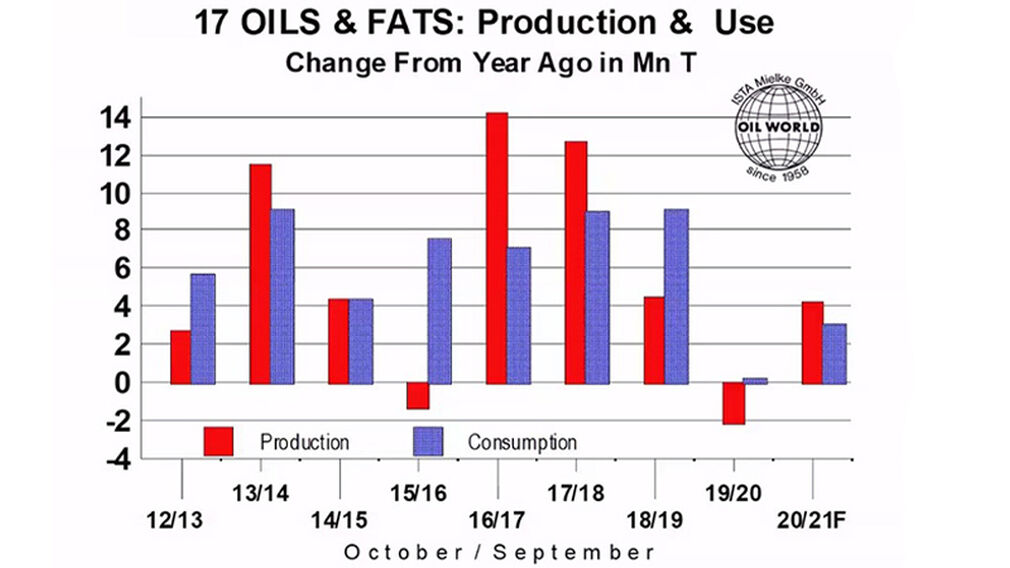

Mielke said world consumption of oils and fats would exceed production for the second consecutive year.

He forecast consumption for October 2020/September 2021 at 240.28M tonnes, against production of 239.77M tonnes. In October 2019/September 2020, consumption was an estimated 237.2M tonnes against 235.49M tonnes of production.

Global vegetable oil stocks were also at unusually low levels with a stock/usage ratio of 12.8%, while biodiesel policies were an uncertainty to watch, he said.

Mielke forecast world biodiesel and HVO production at 47.5M tonnes for 2021 (January-December) against 45.3M tonnes in 2020. Some 17.9M tonnes of palm oil would be used as feedstock for this year’s production, and 12.6M tonnes of soyabean oil, which were large volumes, he said.

His forecast prices for 2021 (January-December) are:

Soyabean oil (Argentina, fob): US$1,100/tonne, with an Oct/Dec average price of US$1,000/tonne.

RBD palm olein (Malaysian fob): US$950/tonne, with an Oct/Dec average price of US$840-880/tonne.

Coconut oil: $1,380/tonne.

PKO: US$1,310/tonne.

“Prices are likely to stay elevated and above average throughout 2021 but weaken from current levels if world production of oilseeds rebounds in 2021/22 on the assumption of higher plantings and normal to favourable weather and a global production surplus becoming likely.”

Godrej International director Dorab Mistry said 2021 would be a year of two halves with the April to June period seeing a tight supply and demand situation.

“The price curve post April-May will be downward. Growing weather will be key and high prices will eventually lead to high production.

“Prices may fall dramatically in July-August if rains are adequate in North America.”

Mistry forecast Bursa Malaysia Derivatives (BMD) palm oil prices staying at Ringitt 3,300 (US$798) up to June, and then bottoming at 2,700 Ringitts (US$653) from July onwards.

He noted that the election of US President Joe Biden had given a huge push to green fuels, particularly biodiesel in the USA. Fossil fuel refineries in the USA were switching to biofuel/HVO production and the market had seen Europe shipping canola oil to Canada because US biodiesel demand was taking up edible oil supplies in North America.

“Canadian canola oil is the safety valve of the US domestic market and rapeseed oil is therefore the most likely candidate to maintain its high price in the second half of 2021.”

LMC International chairman James Fry also noted that Biden’s US$1.9 trillion stimulus package would lead to the return of inflation and higher interest rates, making speculation in commodities less appealing.

He said the vegetable oil market was currently in a bubble.

“La Niña hit all oil crops, pulling vegetable oil supply down below expectations at the start of 2020. Demand has been a bigger surprise. After a sharp shock in the second quarter of 2020, consumption has been well maintained. Far from allowing biodiesel demand to ease and avoid the food versus fuel dilemma, key governments are maintaining or even increasing (in Brazil and Colombia), biodiesel mandates, raising the price of oils for food as a result.

“This inflationary pressure is being increased by the money printing machines, both funding government deficits and helping families survive the income losses triggered by COVID-19. When interest rates are zero, the credit created in the economy has to find a home, and one such home is the commodity market, with buyers hoping to ride the speculative wave.”

Going forward, Fry said high prices would ration food demand and the oil crop output would revive slowly.

“The recovery in Southeast Asian CPO output will leading to a slow rise in palm oil stocks.”

As a result, the EU CPO-Brent crude oil spread should drop from a crazy US$700/tonne now to US$450/tonne by fourth quarter 2021, which would mean EU CPO would settle around US$925/tonne then.

“Allowing for freight and export taxes, BMD would be near RM3,300 (US$798),” he concluded.

{kind=link}