The use of oils and fats for biofuels reached 18% of total world consumption this year while edible use has fallen as a result of high prices, Oil World CEO Thomas Mielke told the Palm Oil Internet Seminar (POINTERS) on 18 October.

“Will a new food vs fuel debate lead to reduced biofuel targets and will this debate become stronger again as edible oil consumers suffer from high prices?” he asked.

Mielke said that 10 years ago, the consumption of oils and fats for biofuels stood at 12%.

Soyabean oil prices were close to US$1,400/tonne on 15 October and palm oil prices were around US$1,300/tonne, double that of crude mineral oil prices.

Despite this, consumption of vegetable oils for biofuel use had increased, with production of biodiesel and hydrotreated vegetable oil (HVO) rising by 1.5M tonnes in 2021 globally, reaching a new high of 48M tonnes.

Mielke said the price boom in vegetable oils had not yet broken, with consumers cutting back on usage - mainly in the edible sector - but farmers boosting oilseed plantings worldwide by 9M ha.

He forecast that world production of the 10 major oilseeds would increase by 24M tonnes to total over 600M tonnes in 2021/22.

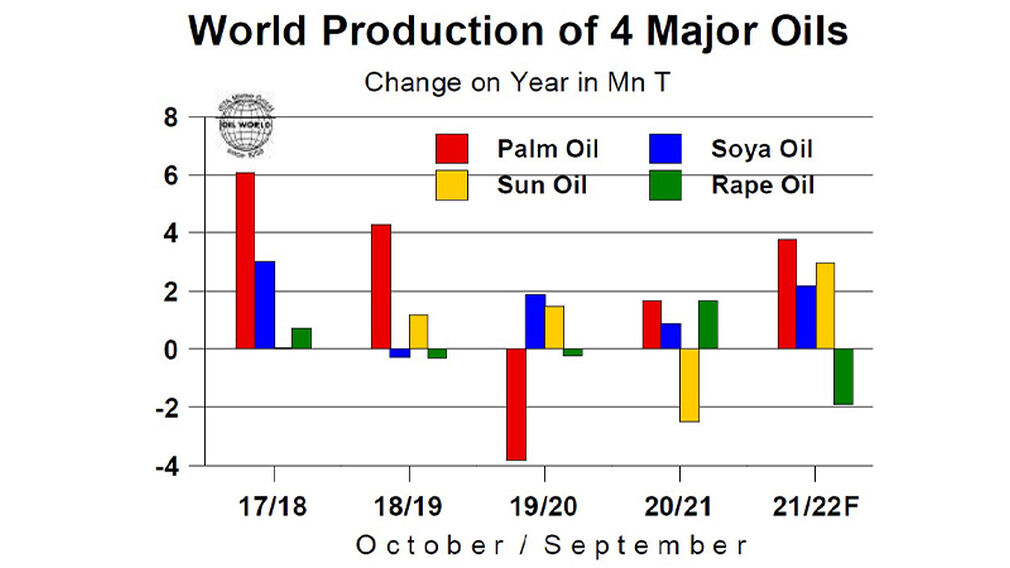

“For 2021/22, we forecast world production of the four major vegetable oils (palm, soyabean, sunflower, rapeseed oils) to increase by about 7M tonnes, the biggest growth in four years.

“This follows two years of a global production deficit and a sharp decline in stocks. If this forecast materialises, vegetable oil prices will start declining and should gain momentum in the course of 2022.”

For palm oil, global production would reach almost 80M tonnes in 2021/22.

However, the sector had experienced a lack of new plantings in the last three years and average annual growth would lag in the next five to 10 years.

Malaysia would see a production increase of 3.5-4M tonnes this year to total 18.2M tonnes but the country’s average annual yield would fall to a 20-year low this year.

Lack of labour was a major constraint but the situation was likely to improve in 2022 if the government’s plan to recruit 32,000 foreign workers materialised.

Soyabean production was set to rise by 17M tonnes in the current 2021/22 season to total 179M tonnes, 62% of world oilseed production.

Production of the crop was now rising faster than consumption and stocks were also set to increase, mainly in the USA and South America.

“But there are still many uncertainties,” Mielke said. This included the weather, COVID effects, purchases by key importing countries like China, currency fluctuations, multi-year energy price highs affecting economic development in many countries, and government policies such as import and export duties and quotas.

South America would see a significant growth in planted area with Brazil forecast to experience a 145M tonnes crop in 2021/22 (against 138M tonnes in 2020/21); and Argentina 46-47M tonnes (against 43.8M tonnes). The USA would also have an increased crop of 121M tonnes compared with 115M tonnes in 2020/21.

World sunflowerseed production had plummeted by 5.3M tonnes in 2020/21 but had experienced a substantial recovery of 4M tonnes, with an expected crop of 57.4M tonnes expected in 2021/22, raising oil export supplies.

Meanwhile, production of rapeseed and canola plummeted to a 13-year low of only 62M tonnes in 2021/22.

“Vegetable oil prices showed remarkable strength in the first half of October,” Mielke said. “The high prices are not sustainable and the stage is set for a recovery in production and stocks.”

Assuming normal weather, Oil World was forecasting global vegetable oil production to increase, stocks to recover and vegetable oil prices to weaken.

“After two years of tightness, world production of oils and fats will increase by about 8M tonnes in 2021/22, which is a four-year high, with most of the growth in palm oil, sunflower oil and soyabean oil.”

{kind=link}